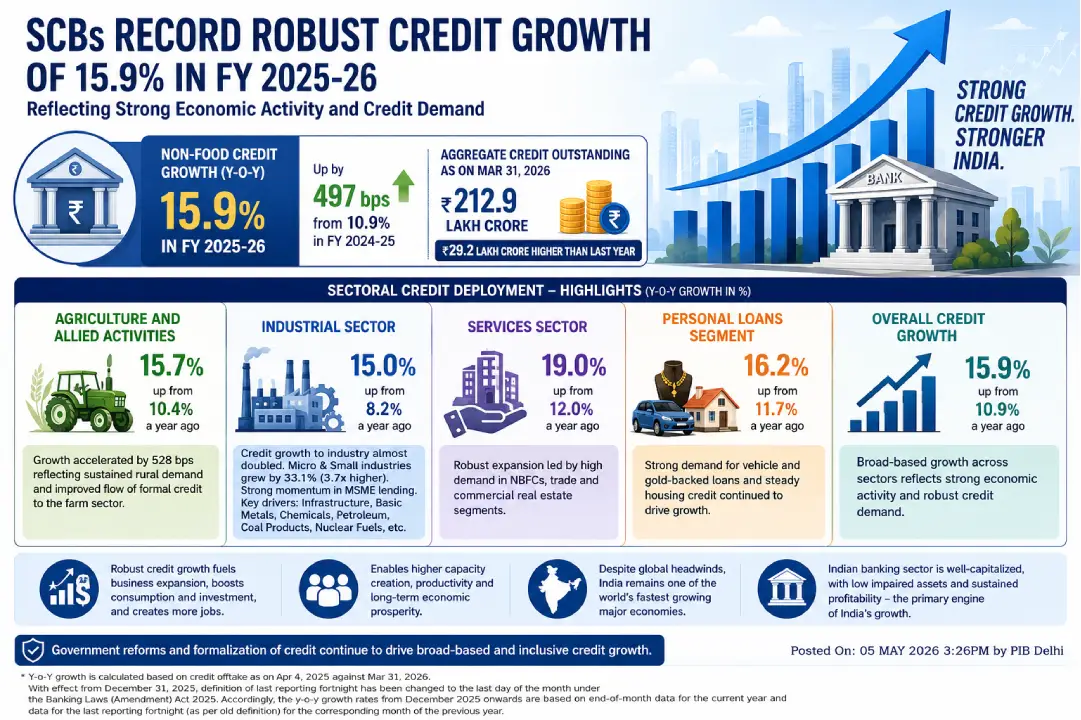

India's Scheduled Commercial Banks recorded 15.9% non-food credit growth in FY 2025-26, adding ?29.2 lakh crore. All sectors — agriculture, industry, services, and personal loans — showed accelerated growth, reflecting strong domestic demand.

India's Scheduled Commercial Banks (SCBs) concluded the financial year 2025-26 on a markedly strong note, recording a non-food credit growth of 15.9% year-on-year — a substantial jump of 497 basis points over the 10.9% growth reported in the same period a year earlier. The aggregate credit outstanding as of March 2026 reached Rs. 212.9 lakh crore, reflecting a Rs. 29.2 lakh crore increase over the previous year. The robust performance signals renewed confidence among both corporate borrowers and individuals in the resilience of the Indian economy.

Credit expansion has been broad-based across all major segments — services, personal loans, agriculture and allied activities, and industry — supported by a low-interest-rate environment, government-aided capital expenditure, structural reforms, and increasing private investments crowding into the economy.

The agriculture and allied sector witnessed a significant acceleration in credit growth, rising to 15.7% in FY 2025-26 from just 10.4% in the preceding year — an increase of 528 basis points. This positive momentum is attributed to sustained rural demand and the progressive formalisation of rural credit channels. Increased policy support for the farm sector and improved last-mile delivery of credit have reinforced confidence among farmers and rural entrepreneurs, contributing to a higher-than-expected uptake of agricultural credit during the year.

Industrial credit recorded one of its sharpest accelerations in recent years, expanding at 15.0% in FY 2025-26 — nearly double the 8.2% growth registered in the previous year. The micro and small industries segment was the standout performer, posting an impressive year-on-year growth of 33.1%, which is 3.7 times the credit growth seen in FY 2024-25. Medium-scale industries also posted healthy expansion, with credit growing by 21.7% year-on-year.

Key drivers of industrial credit growth included sectors such as Infrastructure, Basic Metal and Metal Products, Chemicals and Chemical Products, as well as Petroleum, Coal Products, and Nuclear Fuels. These sectors have benefited from the government's continued focus on capital expenditure and manufacturing-led growth, which is drawing in private investment and enabling firms to expand capacity through investment in fixed assets.

The services sector, which accounts for 28% of overall bank credit, recorded the highest sectoral growth at 19.0% year-on-year, sharply higher than the 12.0% growth seen in the corresponding period of the previous year. Credit demand from Non-Banking Financial Companies (NBFCs), the trade segment, and the commercial real estate sector were the primary contributors to this surge, reflecting growing economic activity and urbanisation-driven investment.

The personal loans segment, which constitutes the largest share of overall bank credit at 33%, expanded by 16.2% in FY 2025-26, up from 11.7% in the previous year — a growth differential of 455 basis points. Strong demand for vehicle loans and loans against gold jewellery sustained the segment's momentum throughout the year, while the housing segment registered steady, consistent growth, underscoring continued consumer confidence in long-term asset acquisition.

India's banking sector remains at the forefront of economic growth, characterised by a well-capitalised balance sheet, historically low impaired assets, and sustained profitability. This financial health enables the banking system to support expanding credit demand without compromising systemic stability. The government's persistent efforts to democratise and formalise credit have resulted in more inclusive and broad-based credit deployment across urban and rural geographies alike.

Against a challenging global backdrop of geo-economic fragmentation and geopolitical pressures, the Indian economy has demonstrated remarkable resilience, maintaining its position as one of the fastest-growing major economies in the world. The robust credit growth of FY 2025-26 reflects this underlying strength, supporting business expansion, job creation, and the sustained acquisition of durable goods by individuals — all of which further accelerate industrial activity and investment in productive capacity.